Copyright © Financial Services Commission, Mauritius. All rights reserved

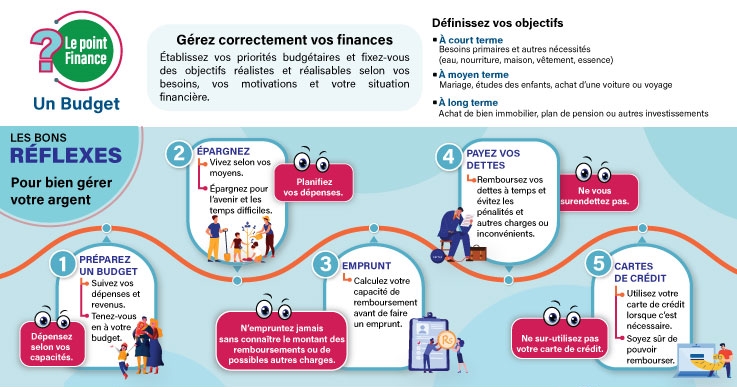

By having a household budget in place, you can easily track your spending, save, and more easily monitor and reach your financial goals.

The first step towards planning your budget is to determine exactly how much money you have coming, including side income. In most households, income will be coming from the job(s) you and your spouse hold. If you have any other income coming in from other sources, such as stocks or a rental of property, be sure to include that in your monthly total as well.

Once you have calculated your total monthly income, you should subtract your necessary fixed expenses from the total. These are expenses you have to pay absolutely each month. This includes bills like your rent, utilities, car payments and insurance premiums. Remember that even items like groceries, while they need to be factored into your budget, are NOT fixed costs. These are variable items that you can adjust when you need to.

After you have subtracted your necessary expenses, you should set a target savings goal out of what is left. This is money you are going to put aside for long term financial goals like building your emergency fund, saving up for buying a house and saving for retirement.

It is important to put your savings aside as soon as you get you pay because otherwise it is very easy to spend everything and not have any money left. Once you decide on a savings target, you may want to schedule automatic transfers to your investment or savings accounts so you will be sure to reach your monthly goals.

Debt plays a bit of a mixed role in a budget allocation. If your accounts require minimum payments, you should consider these as part of your necessary expenses. Missing minimum payments damages your credit score and could lead to expensive penalties so you really need to make these payments on time. From there, a good strategy is to consider paying down your debt as one of the financial goals to be paid out of your monthly savings.

Share this page