Copyright © Financial Services Commission, Mauritius. All rights reserved

The FSC Mauritius regulates private pension schemes so that they comply with provisions of the PPSA. The main objective is to maintain a fair, safe, stable and efficient private pension industry in Mauritius.

Defined Benefit Scheme is where the amount of pension payable to the employee at retirement is linked to a formula to the members’ salaries and length of employment.

Defined Contribution Scheme is where a certain amount or percentage of money is set aside each year by a company for the benefit of each of its employees at retirement. The minimum contribution payable by the employees and/or the employers are fixed in advance, normally as a percentage of salary

Parties are:

Pension Schemes set up under/ as:

• Association registered before the commencement of the PPSA under the Registration of Associations Act

• National Pension Fund (NPF) / National Savings Fund (NSF)

• Civil Service Family Protection Schemes Act

• Statutory Bodies Fund Acts

• Sugar Industry Pension Fund Act

• Local Authorities (Pensions) Act

• Registrar of Association Act

• Individual Pension Plans set up under the Insurance 2005 Act

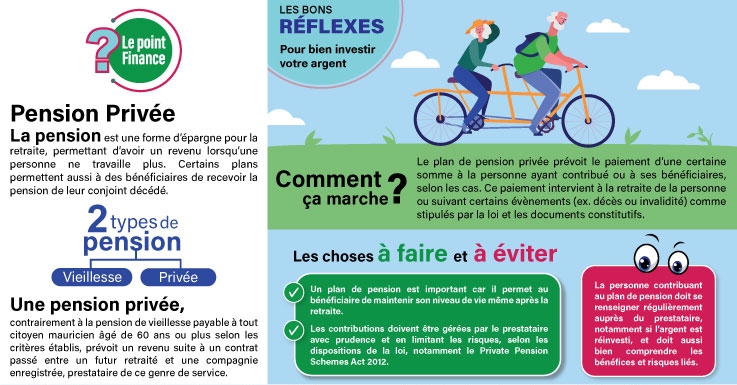

A pension is the monthly income that a person receives once s/he has retired. On reaching retirement age, a person’s main source of income will be her/his pension. Pension benefits can either be in the form of a cash lump sum paid on retirement date, and/or regular payments made as from the retirement date.

A pension scheme is a savings vehicle/structure in which you can save during your working life and which will provide a pension once you retire.

In some circumstances, your employer also contributes for your pension.

A pension is a long term investment. Private Pension Schemes set up by private companies and service providers provide pension benefits to the employees of the sponsoring employers.

A private pension scheme is an arrangement whereby members of the pension scheme are entitled to benefits upon retirement or upon death or termination of employment due to illness or upon the occurrence of such events as specified in law or in the documents establishing the pension scheme.

Important: a pension scheme is not a bank account where you put money in and take out when you want. It is a long term investment and benefits are paid at retirement.

We may think we will never get old but retirement arrives faster than we can imagine. Therefore, saving for your retirement is essential because everyone has to stop working at some point. Although the Mauritian State provides a basic retirement pension to all citizens who reach 60 years old, depending on relevant conditions being observed, it is unlikely that it is going to give you the standard of living you may want or are used to. You can plan for your retirement by being a member of a private pension scheme.

A pension ensures that you are catered for financially when you have retired. It is recommended to start saving into a pension scheme as soon as possible to ensure you have the standard of living you want when you retire. Therefore, if you want a reasonable income, you must start saving for your retirement as early as possible. The earlier you start the better because it is cheaper to save over a longer period of time as you will end up with more money put aside to provide for your pension.

You can invest in a pension scheme: