Copyright © Financial Services Commission, Mauritius. All rights reserved

Home » Financial Technologies » Peer to Peer Lending

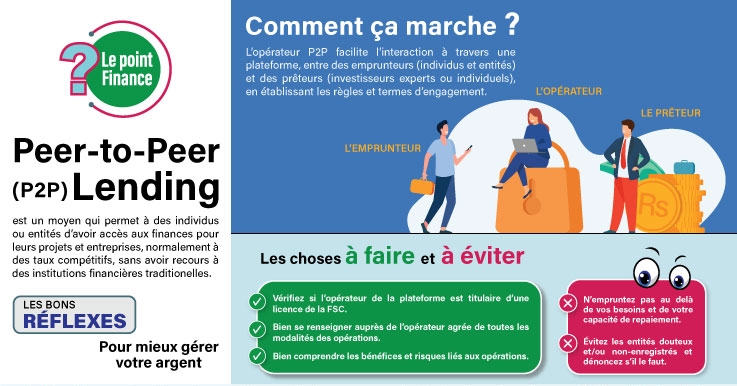

The Rules provide a sound and efficient regulatory environment to support the conduct of Peer to Peer (P2P) Lending for the benefits of stakeholders in the non-bank financial services sector of Mauritius. The P2P Lending framework will enable eligible individuals and entities to access market-based financing to fund their projects or businesses via an online platform.

Peer to Peer Lending Operators (‘P2P Operators’), licensed by the FSC Mauritius, facilitate the access to finance by matching individuals and entities (borrowers) and retail and expert investors (lenders), through P2P lending platforms.

Lenders:

Lenders in P2P Lending can be both an individual and a company.

Borrowers:

P2P Lending is open to individuals or entities.

The following types of schemes & entities will not be entitled to borrow pursuant to the P2P Lending Rules.

P2P Operators:

Operators of P2P lending platforms must be licensed by the FSC Mauritius to facilitate interactions between the demand (borrowers) and supply (lenders).

The costs and charges applied by P2P operators may vary according to the business model of the P2P lending platform.

The rate of returns received by Lenders from P2P Lending will inter-alia depend on the Borrower’s risk of default and the terms of the project financing.

Only a P2P operator licensed by the FSC Mauritius can operate a P2P Lending platform. A P2P operator must be a company incorporated under the Companies Act 2001 and must maintain a minimum unimpaired stated capital of MUR 2 million or its equivalent in any other currency, or such higher amount as may be determined by the FSC Mauritius. A P2P operator must ensure that funds obtained from Lenders are placed in a segregated bank account with a licensed financial institution in Mauritius, until the appropriate disbursements are made.

A P2P operator will be restricted from undertaking certain activities in its own name, namely those of:

o Deposit taking business, in any form;

o Lending; and

o Providing or arranging for any credit enhancement or guarantee.

Lender

Individuals shall not lend more than MUR 1.5 million (in the aggregate) through P2P Operators in any 12 months period; and

Entities shall not lend more than MUR 3 million (in the aggregate) through P2P Operators in any 12 months period.

A borrower

Individuals shall not borrow more than MUR 1 million (in the aggregate) through P2P Operators, at any time until at least one third of the amount borrowed is reimbursed; and

Companies shall not borrow more than MUR 5 million (in the aggregate) through P2P Operators, at any time until at least one third of the amount borrowed is reimbursed.

All funds transacted through P2P Lending platforms are not tantamount to bank deposits or credits in Mauritius and therefore, there shall not be any statutory compensation in case of loss on P2P Lending platforms.

The P2P operators are subject to the requirements set out in the Financial Services Act 2007 , the P2P Lending Rules and other legislations which may include the following:

o A P2P operator must be a company incorporated under the Companies Act 2001 and maintain a minimum unimpaired stated capital of MUR 2 million or its equivalent in any other currency, or such higher amount as may be determined by the FSC Mauritius.

o The P2P operator will be required to be managed by a Board consisting of a minimum of three directors, one of whom shall be a resident and independent director in Mauritius.

o A P2P operator will also be required to establish an office and have in place appropriate Information Technology infrastructure to carry out its business activities within Mauritius.

Application for a licence as P2P operator must be submitted online, through the FSC One Platform. Details of the licensing criteria are published on the website of the FSC Mauritius.

Share this page